Changing jobs is exciting—a new role, fresh opportunities, and a chance to grow. But have you thought about what happens to your 401(k)? Surprisingly, nearly 25% of Americans leave their 401(k) behind and unwatched during a job change, risking fees, penalties, or even forgotten savings.

Your 401(k) represents years of hard work and savings. By making the right decision now, you can keep your retirement plans on track and maximize your financial potential. Let’s explore your options to help you make the smartest choice.

Why You Need a Plan for Your Old 401(k)

Leaving your 401(k) unaddressed when transitioning to a new job can lead to:

- Missed Opportunities: Losing access to better investment options or lower fees.

- Unnecessary Fees: Many old plans have hidden costs that reduce your savings.

- Forgotten Accounts: Without proper tracking, these accounts can fall by the wayside, impacting your retirement strategy.

Take Action Today: Don’t let your 401(k) become an afterthought. Schedule a complimentary consultation with FSC Wealth Advisors to assess your options.

Schedule Now

4 Smart Options for Managing Your 401(k)

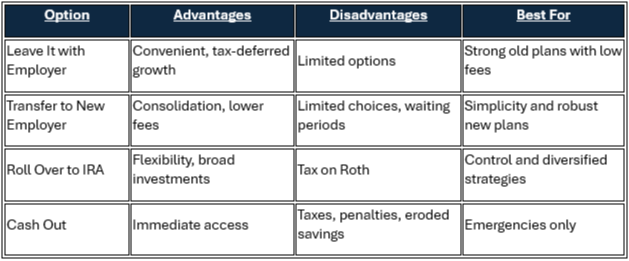

Option 1: Leave It with Your Former Employer

Advantages:

- No immediate action required.

- Savings continue to grow tax-deferred.

Disadvantages:

- Limited control over investment options.

- Potential fees and restricted access.

- Risk of automatic distributions for small balances.

When It Makes Sense: If your old plan offers low fees and strong investment options, this might be a temporary solution. But don’t forget about it, remember to review it annually to avoid neglecting your savings.

Real-World Example:

Sarah left her 401(k) with her former employer because it had excellent investment options and low fees. She set reminders to review the account annually, ensuring it stayed in line with her larger financial plan

Option 2: Transfer It to Your New Employer’s Plan

Advantages:

- Accounts are consolidated for easier management.

- May offer lower fees or better investment choices.

Disadvantages:

- Limited investment options in some plans.

- Potential waiting periods or restrictions.

How to Do It:

- Direct rollover to avoid taxes and penalties.

- Compare the investment options and fees in your new employer’s plan.

When It Makes Sense: This is a great option if your new employer’s plan has robust features and you value simplicity in managing your accounts.

Option 3: Roll Over to an IRA

Advantages:

- Access to a wider range of investments.

- Greater control over your retirement strategy.

- Tax-deferred growth (or tax-free growth with a Roth IRA).

Disadvantages:

- Potentially higher fees than employer-sponsored plans.

When It Makes Sense: Rolling over to an IRA is ideal if you want flexibility and broader investment choices.

Option 4: Cash Out Your 401(k)

Advantages:

- Immediate access to funds if needed urgently.

Disadvantages:

- Subject to income taxes and penalties if under 59½.

- Significantly erodes your retirement savings.

When It Makes Sense: This option should only be considered in emergencies or unavoidable financial hardships.

Warning:

Cashing out should be a last resort. Taxes and penalties can quickly deplete your savings.

Factors to Consider

When deciding what to do with your old 401(k), keep these factors in mind:

- Age and Timeline: Younger investors may prioritize growth, while retirees may focus on stability.

- Current Financial Needs: Balance immediate access to funds with long-term goals.

- Investment Options and Fees: Compare your current plan with alternatives like IRAs.

- Professional Guidance: Consult a financial advisor to weigh your options.

Pro Tips for a Smooth Transition

- Avoid Penalties: Always use direct rollovers to prevent taxes and penalties.

- Stay Organized: Keep track of all accounts and consider consolidating when appropriate.

- Review Your Strategy: Changing jobs is a perfect time to reassess your financial plan and ensure your savings align with your plan.

Your 401(k) is more than just another account—it’s a key part of your financial future. Whether you leave it with your former employer, roll it over, or consolidate with a new plan, making an informed decision is critical.

Take the Next Step:

Schedule a complimentary consultation with FSC Wealth Advisors today to create a tailored strategy for your retirement savings.

| About the Author |